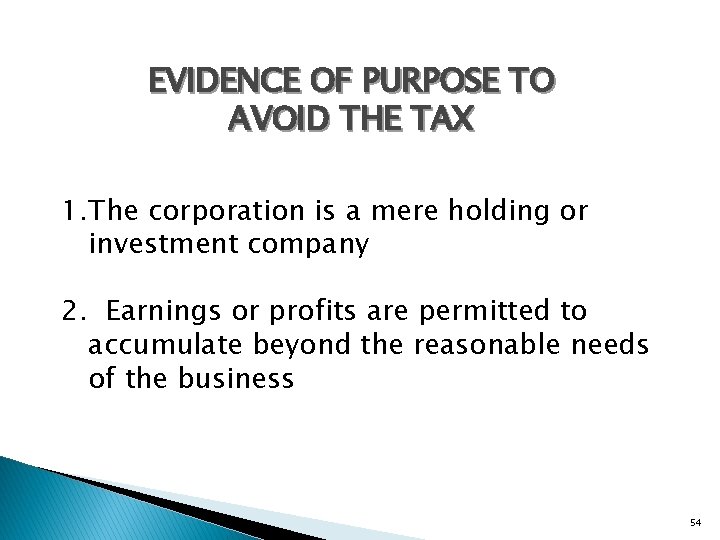

accumulated earnings tax reasonable business needs

This taxadded as a penalty to a companys income tax liabilityspecifically applies to the companys taxable income less the deduction for dividends paid and a standard accumulated tax credit of 250000 150000 for personal service corporations. Save Time Track Money And Get Important Insights With Easy Expense Tracking.

Prepared By Lilybeth A Ganer Revenue Officer Ppt Download

The accumulated earnings tax imposed by section 531 shall apply to every corporation other than those described in subsection b formed or availed of for the purpose of avoiding the income tax with respect to its shareholders or the shareholders of any other corporation by permitting earnings and profits to accumulate instead of being divided or distributed.

. An accumulation of the earnings and profits l is in excess of the reasonable needs of the business if it exceeds the amount that a prudent businessman would consider appropriate for the present business purposes andfor the reasonably anticipated future needs of the business. Ad Talk to a 1-800Accountant Small Business Tax expert. When the PHC tax applies there is relief from the accumulated earnings tax Section 532a b1.

A corporation is liable for the AET when it accumulates does not distribute earnings beyond the greater of 250000 or Reasonable business needs. An IRS review of a business can impose it. Earnings and profits is not the same as a corporations taxable income.

The tax equals 20 of accumulated undistributed taxable income. We have the experience and knowledge to help you with whatever questions you have. The tax is in addition to the regular corporate income tax and is assessed by the IRS typically during an IRS audit.

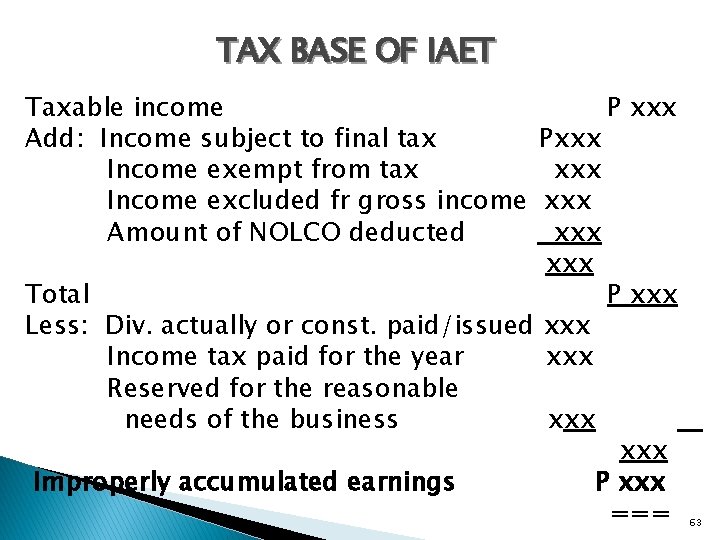

Within the reasonable needs of the business rubric. 5 1537-1 states in part. Taxable Income - Adjustments Current EP.

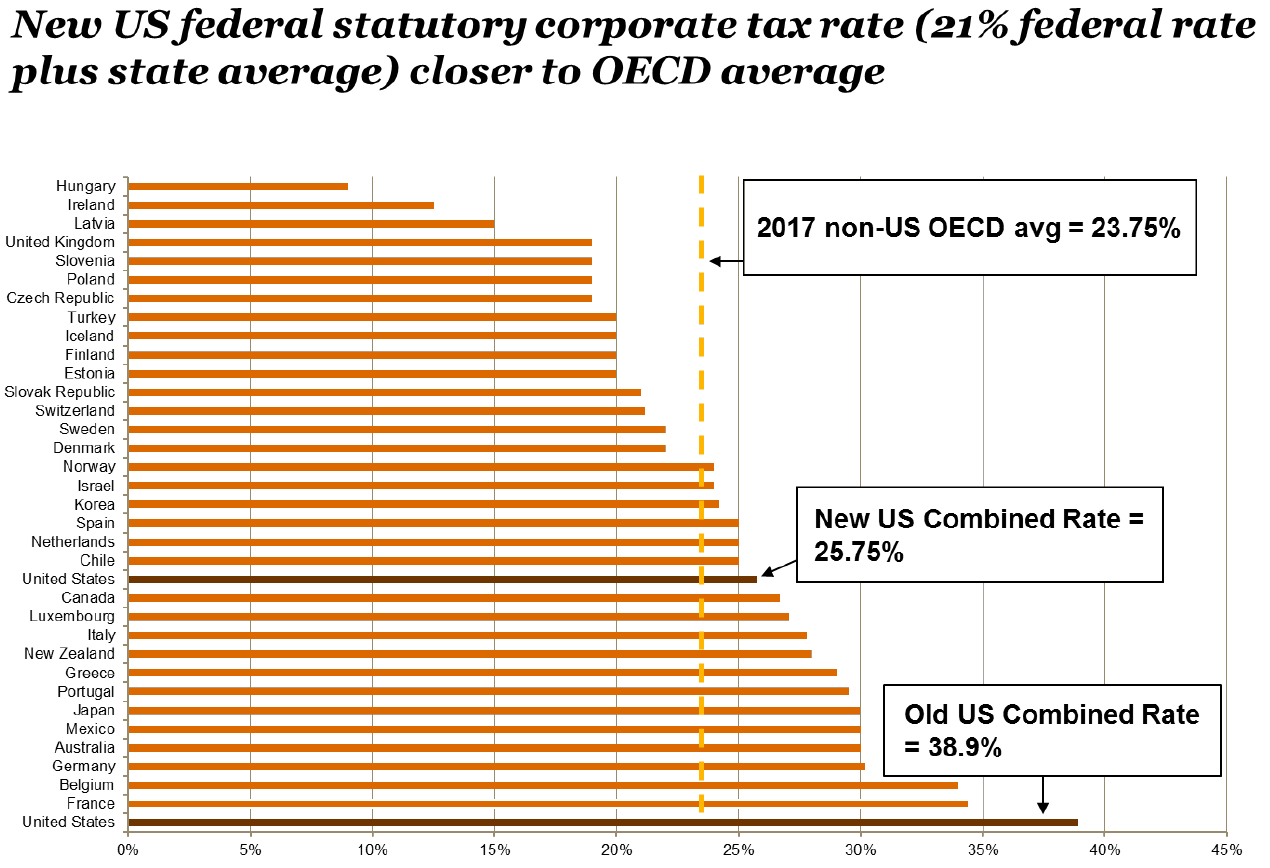

The accumulated earnings tax equals 396 percent of accumulated taxable income and is in addition to the regular corporate tax. However this opens the door to the Accumulated Earnings Tax AET if profits accumulate beyond the reasonable needs of the business. The AET is a penalty tax imposed on corporations for unreasonably accumulating earnings.

Ad Track Your Expenses Easily With QuickBooks - Highly-Rated Tracking Software. If a C corporation retains earnings doesnt distribute them to shareholders above a certain amount an amount which the IRS concludes is beyond the reasonable needs of the business the corporation may be assessed tax penalty called the accumulated earnings tax IRC section 531 equal to 20 percent 15 prior to. Business expansion constructing a new facility and investing in newer and more productive equipment are reasonable business needs.

The unreasonable accumulation of earnings and nonpayment of dividends. WHAT ARE THE REASONABLE NEEDS OF THE BUSINESS. Keep in mind that this is not a self-imposed tax.

The fact that a corporation accumulates earnings beyond the reasonable needs of its business is determinative of a purpose to avoid shareholder income tax unless the corporation proves to the contrary by a preponderance of the evidence see Regs. Liability for the accumulated earnings tax is based on the following two conditions. The PHC tax is self-imposed.

But because Section 533a provides that the existence of accumulations of earnings beyond the reasonable needs of the business establishes a presumption in favor of. The tax rate on accumulated earnings is 20 the maximum rate at which they would be taxed if distributed. Accumulated Earnings Tax IRC 531 The purpose of the accumulated earnings tax is to prevent a corporation from accumulating its earnings and profits beyond the reasonable needs of the business for the purpose of avoiding income taxes on its stockholders.

THE ACCUMULATED EARNINGS TAX AND THE REASONABLE NEEDS OF THE BUSINESS. The purpose of the tax The purpose of accumulated earning tax is to discourage the accumulation of profits if the purpose of such accumulation is to enable shareholders to avoid paying taxes on those profits by not paying them dividends. Relative to the accumulated earnings tax explain what reasonable business needs means and give 3 examples of what the IRS would likely accept as reasonable.

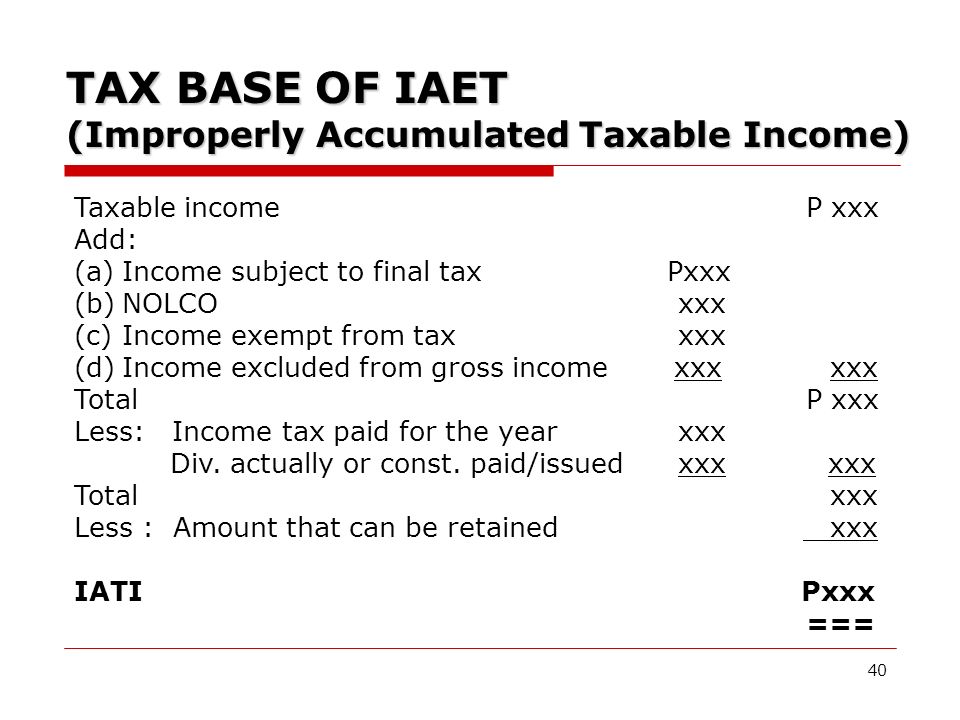

1 Accumulated taxable income is taxable income modified by adjustments in 535 b and as reduced by the dividends paid deduction under 561 and the accumulated earnings tax credit under 535 c. The IRS and corporations can and do find themselves battling in the US. 1 Accumulated taxable income is taxable income modified by adjustments in 535 b and as reduced by the dividends paid deduction under 561 and the accumulated earnings tax credit under 535 c.

The amount of current year earnings and profits that are retained for reasonable business needs in excess of dividends paid to the shareholders less the net capital gains deducted in calculating accumulated taxable income. And profits have been allowed to accumulate beyond the reasonable. The accumulated earnings tax has been referred to as a penalty on success itself Of all the taxes imposed upon business this is probably one of the most unpopular involving an after the fact verdict on manage-ments business judgment.

The primary defense usually levied by the corporation is that the accumulated earnings beyond 25000000 were essential to the reasonable needs of the business. S corporations dont have a problem with accumulated earnings because earnings are taxed to S corporation shareholders even if theyre not distributed to them. Get the tax answers you need.

533 - 1 a 1. Relative to the accumulated earnings tax explain what reasonable business needs means and give 3 examples of what the IRS would likely accept as reasonable business needs. Given the reasonable needs of the business part of the tax calculation put ten around a table to figure the tax youd likely get ten different answers.

Accumulated earnings can be reduced by dividends actually or deemed paid and corporations are entitled to an accumulated earnings credit which will be the greater of 1 a minimum of a 250000 lifetime credit for most corporations 150000 in the case of a corporation whose principal function is the performance of health legal engineering. A General rule For purposes of this part the term reasonable needs of the business includes 1 the reasonably anticipated needs of the business 2 the section 303 redemption needs of the business and 3 the excess business holdings redemption needs of. To avoid having to pay for accumulated earnings tax Company A has to distribute at least 100000 of net income as dividends.

Tax Court over the imposition of the accumulated earnings tax. Use the IRS Online Tax Calendar.

Darkside Of C Corporation Manay Cpa Tax And Accounting

Income Tax Computation Corporate Taxpayer 1 2 What Is A Corporation Corporation Is An Artificial Being Created By Law Having The Rights Of Succession Ppt Download

Understanding The Accumulated Earnings Tax Before Switching To A C Corporation In 2019

Overview Of Improperly Accumulated Earnings Tax In The Philippines Tax And Accounting Center Inc

Corporate Distributions

2

Prepared By Lilybeth A Ganer Revenue Officer Ppt Download

Improperly Accumulated Earnings Mpcamaso Associates

:max_bytes(150000):strip_icc()/debtequityratio.asp_FINAL-0ac0c0d22215418a992fa7facd2354e6.png)

Debt To Equity D E Ratio Definition

Test Bank Income Taxation Cpar

/GettyImages-1130199515-b011f8c58a144789b22c7107929ffb8f.jpg)

Accumulated Earnings Tax Definition

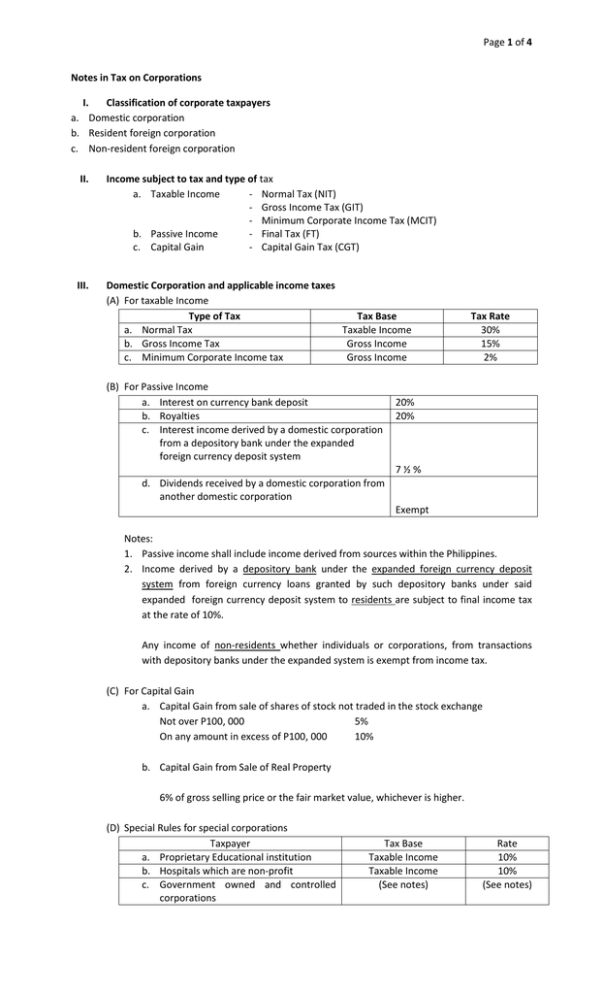

Notes In Tax On Corporations

Income Tax Computation For Corporate Taxpayers Prepared By

Income Tax Computation For Corporate Taxpayers Prepared By

Income Tax Computation For Corporate Taxpayers Prepared By

Income Tax Computation For Corporate Taxpayers Prepared By

Doing Business In The United States Federal Tax Issues Pwc

Quizzer Tax Part 2 Partnership And Corporation Pcba Cpa Review Concordia Sur Nueva Valencia Studocu

Income Tax Computation Corporate Taxpayer 1 2 What Is A Corporation Corporation Is An Artificial Being Created By Law Having The Rights Of Succession Ppt Download